If you’ve ever wondered how businesses accept payments from credit cards, debit cards, or digital wallets, the answer usually starts with something called a merchant account.

Whether you’re shopping online, dining at a local cafe, or booking a subscription for a streaming service, a merchant account is working quietly behind the scenes to transfer your money from your card to the business’s bank account.

In this guide, you’ll get the full picture: what a merchant account actually is, how it works, why businesses need one, and what you should know before choosing a provider.

Whether you’re launching an e-commerce store, opening a physical shop, or simply curious about how payment systems connect globally, this article covers it all.

Let’s get started!

What is a Merchant Account?

A merchant account is a type of business bank account that allows you to accept credit card payments and other types of electronic payments. It acts as an intermediary between your customer’s bank and your business’s bank account.

Here’s how it works in simple terms:

- A customer makes a payment using a credit or debit card.

- The payment is routed through a payment processor and a payment gateway (for online sales).

- The funds first land in your merchant account.

- After a short holding period (typically 1-3 business days), the funds are released into your business’s bank account.

Checkout: Payment Processor vs. Payment Gateway [2025]

Without a merchant account, businesses wouldn’t be able to process transactions directly from major card networks like Visa, Mastercard, Discover, or American Express.

This type of account is different from a regular checking account because it’s designed specifically for handling the movement of electronic funds. It’s governed by payment networks and subject to specific security standards.

Why Businesses Need a Merchant Account

In 2024, over 60% of all retail transactions in the U.S. were made using credit or debit cards, according to the Diary of Consumer Payment Choice Report by The Federal Reserve. With this growing reliance on card payments, having a merchant account isn’t simply not an option anymore but a requirement for long-term success.

Here are some of the top reasons why you need one:

- To accept credit card payments — in-store, online, or via mobile.

- To increase customer trust — most people feel more comfortable buying from businesses that accept cards.

- To streamline payments — it makes transit into your business bank account smoother.

- For recurring payments — it helps with recurring billing, subscriptions, and invoices.

Getting a merchant account for a small business can feel intimidating, but there are providers who specialize in this space, offering affordable, easy-to-understand plans without long-term commitments.

Whether you’re running a food truck or a SaaS platform, accepting card payments directly improves your cash flow and enhances the customer experience.

How Does a Merchant Account Work? (Step-by-Step Breakdown)

Understanding how a merchant account works helps you see the full journey of a customer’s payment—from swipe or click to the final deposit into your business bank account. It may seem complex at first, but it is generally not, once you understand the dynamics completely.

Here’s a Step-by-Step Payment Flow:

- Customer Initiates a Payment: Whether online, in-store, or via mobile, a customer initiates the payment by entering card details or tapping their card.

- Payment Gateway Captures the Data: If it’s an online transaction, a payment gateway encrypts the card details and transmits them securely to the payment processor.

- Payment Processor Gets to Work: The payment processor routes the transaction through the customer’s credit card network (Visa, MasterCard, etc.) and contacts the issuing bank.

- Authorization is Requested: The issuing bank (your customer’s bank) verifies the card, checks available funds or credit, and either approves or declines the transaction — usually within seconds.

- Funds Go to Your Merchant Account: If approved, the transaction amount is held in your merchant account temporarily while final verifications take place.

- Settlement Happens: Within 1–3 business days, the funds are transferred from the merchant account into your business bank account after deducting the processing fees.

Why This Process Matters

This workflow not only handles money movement but also layers in fraud protection, encryption, and chargeback management. That’s why a merchant account isn’t just a digital vault but a part of a larger payment infrastructure that keeps transactions flowing smoothly and securely.

By understanding the behind-the-scenes process, you can better troubleshoot issues, lower risks of chargebacks, and even reduce fees by optimizing how your transactions are processed.

Difference Between a Merchant Account and a Business Bank Account

At first glance, the two might seem interchangeable, but they serve entirely different roles. The side-by-side chart below can help understand the differences better:

| Feature | Merchant Account | Business Bank Account |

| Purpose | Accepts card payments from customers | Stores funds for business expenses |

| Transaction Role | Temporary holding and settlement | Long-term money storage |

| Direct Customer Use? | No | No |

| Linked to Payments? | Yes (Credit/Debit/Online Payments) | Sometimes (for deposits, not for direct sales) |

In simple words, a business bank account is where your company’s funds live, while a merchant account is where card payments are captured and cleared.

💡 You might want to read this: Merchant Account vs. Payment Gateway: Comparison (2025)

Types of Merchant Accounts (And Which One You Need)

Now that you understand the differences between the two, let’s understand the common types of merchant accounts.

Depending on your business model, risk level, and how you accept payments, there are several different types of merchant accounts available. Choosing the right one can save you money, reduce friction, and help you grow faster.

Let’s break down the most common types — and which type of merchant account fits your business best.

- Retail Merchant Account (For Brick-and-Mortar Stores)

If you run a physical storefront, such as a coffee shop, clothing boutique, or a restaurant, you’ll need a retail merchant account. These accounts are optimized for in-person transactions, where the customer physically swipes, taps, or inserts their card.

Best for: Restaurants, salons, retail shops, repair services

Hardware used: POS terminals, card readers

Lower risk & lower fees due to face-to-face authentication

- E-commerce Merchant Account (For Online Stores)

As the name suggests, an e-commerce merchant account is designed for businesses that sell online, through platforms like Shopify, WooCommerce, BigCommerce, or custom websites. Because the card is not present during these transactions, online accounts are considered slightly riskier comparatively.

Best for: Online retailers, digital products, dropshippers.

Requires: SSL certificates, payment gateway integration, PCI compliance.

Typically has higher fees due to fraud risks

- MOTO Merchant Account (Mail Order/Telephone Order)

MOTO stands for Mail Order / Telephone Order, and this type of account is ideal for businesses that accept card payments over the phone or through catalog-based sales.

Best for: Call centers, B2B sales teams, remote services

Requires: Manual entry system and strong customer verification process

- High-Risk Merchant Account

Some businesses operate in industries considered “high risk” by banks and payment processors — due to a higher likelihood of chargebacks, regulatory scrutiny, or inconsistent income. These businesses need a high-risk merchant account to legally process payments.

Best for:

- CBD or vape sellers

- Adult content platforms

- Gambling or betting sites

- Forex trading services

- Subscription-based services with a refund history

It has higher fees, stricter rules, but more flexibility on global transactions or high volumes.

If you’ve been declined for a regular merchant account, a high-risk provider may still be able to support you — though at a cost.

- International Merchant Account

International merchant account supports multi-currency processing that helps sell to audience internationally and often integrates with global payment methods (like iDEAL in the Netherlands or Alipay in China).

Best for:

- Global e-commerce brands

- Digital downloads

- SaaS companies with worldwide customers

It also comes with currency conversion features, fraud monitoring, and international tax reporting.

Which Type of Merchant Account is Right for You?

Can’t decide on what to choose?

The following chart can help make the best pick:

| Business Type | Best Merchant Account Type |

| Physical retail store | Retail Merchant Account |

| Online-only e-commerce store | E-commerce Merchant Account |

| Phone/catalog sales | MOTO Merchant Account |

| Regulated/high-risk industry | High-Risk Merchant Account |

| Global customer base | International Merchant Account |

By picking the right account type upfront, you can avoid unnecessary fees, get better fraud protection, and receive faster approvals when onboarding with a merchant account provider.

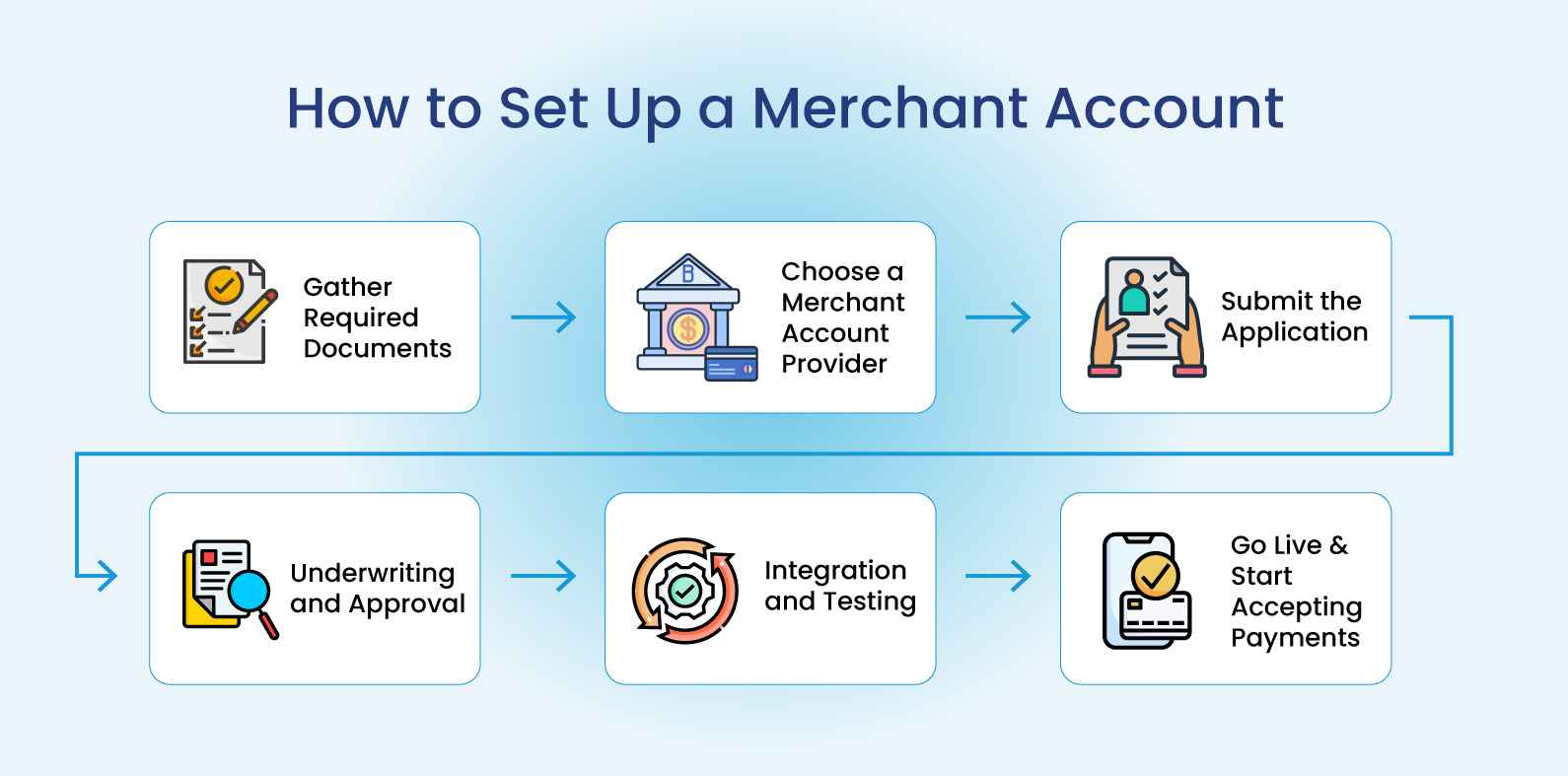

How to Set Up a Merchant Account (Step-by-Step Guide)

Setting up a merchant account might sound complicated at first, but the process is very straightforward. Whether you’re applying for a merchant account for a small business or for a fast-growing e-commerce operation, this step-by-step guide will walk you through it.

The approval process generally takes anywhere from a few hours to a few business days, depending on your provider and the complexity of your business.

Step #1: Gather Required Documents

Before you apply, it’s smart to have all your documentation ready. Here’s what most merchant account providers will ask for:

- Business license or proof of registration (LLC, Sole Proprietor, etc.)

- Employer Identification Number (EIN) from the IRS

- Voided business check or bank letter (to connect your merchant account to your business bank account)

- Government-issued ID (passport, driver’s license)

- Business bank account details

- Recent bank statements (usually 3 months)

- Processing history, if switching from another provider

- Product or service information (website, refund policy, pricing structure)

Pro Tip: For online businesses, your website should already be live and clearly list your products, pricing, privacy policy, and return/refund terms.

Step #2: Choose a Merchant Account Provider

Next, you’ll need to choose a provider based on your business model, transaction volume, industry type, and budget. Some providers specialize in high-risk merchant accounts, while others are built for e-commerce or retail businesses.

Key Features to Compare:

- Transaction fees (flat rate vs. interchange-plus)

- Monthly/annual fees

- Setup and termination fees

- Contract length and cancellation terms

- Customer support availability

- Integration with your website or POS system

- PCI compliance support

Popular merchant account providers include: Helcim, Chase Payment Solutions, Stax, PaymentCloud, and National Processing — each catering to different needs.

Step #3: Submit the Application

Most providers allow you to apply online. During the application, be honest about your:

- Industry category

- Average monthly processing volume

- Average ticket size

- Type of transactions (in-person, online, phone orders, etc.)

This information helps the provider assess risk and tailor their services to your business. For example, if you’re applying for a high-risk merchant account, disclosing that upfront can speed up the underwriting process.

Step #4: Underwriting and Approval

Once submitted, your application enters underwriting. This is the provider’s due diligence phase. They’ll verify your documents, analyze your business model, and assess your risk level (based on industry, chargeback potential, etc.).

Depending on the complexity of your business:

- Low-risk businesses (like retail stores or low-volume e-commerce) may be approved within 24–48 hours.

- High-risk merchants (like CBD sellers, adult content, or subscription services) could take 5–10 business days for review.

Step #5: Integration and Testing

Once approved, you’ll receive:

- Merchant ID (MID)

- Access to your merchant dashboard

- Instructions for connecting to your POS or shopping cart

If you’re using a payment gateway like Authorize.Net or NMI, your provider will assist in linking it to your merchant account. For all-in-one platforms like Stripe or Square, this is handled internally.

Make sure to test your checkout system before going live. By system, we mean everything that facilitates a successful transaction, including payment authorizations, confirmations, and settlements, etc. Lastly, don’t forget to test the payment gateway.

Step #6: Go Live and Start Accepting Payments

You’re now ready to start accepting payments!

Customer transactions will flow through your payment gateway, land in your merchant account, and eventually reach your business bank account. The process usually takes just 1–3 business days.

Getting approved is just the beginning. In the next section, we’ll talk about what it costs to keep your merchant account running, including hidden fees you’ll want to watch out for.

Merchant Account Fees and Pricing Explained

One of the most important—and often most confusing—parts of setting up a merchant account is understanding the fees involved. While many providers advertise “low rates,” the truth is that the pricing structure varies significantly depending on the provider, business type, industry risk, and volume.

Let’s break it all down so you know exactly what to expect and how to avoid getting caught off guard by hidden costs.

- Transaction Fees (Per-Sale Charges)

Every time you process a credit or debit card payment, you’ll pay a transaction fee. This typically includes:

- Interchange fee (set by the card networks like Visa/Mastercard)

- Assessment fee (also from the card networks)

- Processor markup (what your merchant account provider charges)

Average transaction fees:

- In-person payments: 1.5% to 2.6%

- Online payments: 2.3% to 3.5%

- High-risk industries: 3.5% to 6%

The total fee is often expressed as a percentage of the transaction + fixed amount. Example: 2.9% + $0.30 per transaction (like PayPal or Stripe)

- Monthly Fees

Some merchant service providers charge a monthly account maintenance fee, typically ranging from $10 to $30. This covers:

- Customer support access

- Account reporting tools

- Basic PCI compliance features

Not all providers charge this, especially flat-rate platforms like Square.

- PCI Compliance Fee

If you’re accepting credit cards, you must follow the PCI DSS (Payment Card Industry Data Security Standards). Some providers help you become compliant, but others charge a PCI compliance fee, which may be:

- $10 to $25/month or even $100

- Annual fee of around $79 to $120

Non-compliance could also lead to penalties, often $19.95/month or more until the issue is resolved.

- Chargeback Fees

When a customer disputes a transaction, your business may face a chargeback fee, regardless of the outcome. This fee compensates the processor for handling the dispute.

Don’t Miss: Understanding Payment Chargeback: What Merchants Need to Know

- Typical chargeback fees: $20 to $50 per case

- High-risk merchants may face even higher fees

- Excessive chargebacks can jeopardize your merchant account

- Setup & Termination Fees

Depending on your provider, there may be:

- One-time setup fee (up to $100)

- Early termination fee (ETF) — if you cancel before your contract ends. Some contracts charge up to $500 for early cancellation.

Pro tip: Look for no-contract or month-to-month providers like Helcim or Payment Depot to avoid termination fees.

- Batch Fees

A batch fee applies when your provider settles (or “batches out”) your transactions at the end of the day.

- Usually $0.10 to $0.30 per batch

- Daily fee, regardless of transaction volume

- Miscellaneous/Hidden Fees

Here are some less obvious fees that can quietly add up:

- Gateway fee: If using a third-party payment gateway ($5–$15/month)

- Minimum monthly processing fee: Charged if you don’t meet a transaction threshold

- Statement fee: $5–$10/month for mailed paper statements

- AVS/CVV fee: Fraud prevention tools (pennies per transaction)

How to Reduce Merchant Account Costs

- Use interchange-plus pricing instead of tiered pricing for better transparency.

- Avoid contracts with long-term commitments and steep cancellation fees.

- Opt for a provider with no monthly minimums if your volume fluctuates.

- Ask for custom pricing if you process over $10,000/month.

- Monitor your effective rate (total fees divided by sales) to track real costs.

Understanding your fee structure is key to protecting your bottom line. Don’t just look at the headline rate — read the fine print, ask questions, and choose a provider that fits your actual sales model.

How to Choose the Right Merchant Account Provider

With hundreds of merchant account providers out there, choosing the right one can feel like comparing apples to oranges — especially when each company promises low rates and “fast approvals.” But don’t let the marketing noise confuse you. Your merchant account provider plays a central role in how your business handles money, customer trust, and long-term scalability.

Let’s break down how to evaluate merchant account providers, what red flags to watch for, and which features matter most depending on your industry and business model.

Understand Your Business Type and Needs

Different businesses have different processing needs. A SaaS company, for example, has very different payment requirements than a retail shop and vice versa.

To understand your requirements completely, you may ask yourself:

- Will I accept payments in person, online, or over the phone?

- Am I a high-risk merchant (e.g., adult content, supplements, dropshipping)?

- Do I need to support recurring billing or subscriptions?

- How much do I process each month?

Look for Transparent Pricing

Avoid providers that advertise only teaser rates or bury fees in dense contracts.

Instead, look for:

- Interchange-plus pricing (transparent and cost-effective)

- No hidden monthly fees or minimums

- Simple fee breakdowns (e.g., flat per-transaction fees)

- Publicly listed pricing or online calculators

Some reputable providers known for pricing transparency include:

Review Contract Terms Carefully

Many providers try to lock businesses into multi-year contracts with early termination fees (ETFs) or liquidated damages clauses. Look for the following red flags:

- Contracts longer than 12 months

- ETF greater than $250

- Auto-renewal clauses hidden in the fine print

What to look for instead:

- Month-to-month contracts

- No cancellation penalties

- Easy exit process if your needs change

Evaluate Integration Options

Your merchant account should integrate smoothly with:

- Your POS system (like Square Register, Clover, or Vend)

- Your eCommerce platform (like Shopify, WooCommerce, Magento)

- Your payment gateway (like Authorize.net, NMI, or Stripe)

Some providers bundle merchant accounts and gateways, while others let you bring your own. Choose what makes the most sense for your tech stack.

Make Sure They Support PCI Compliance

A good provider should help you stay PCI DSS compliant — ideally with:

- Guided self-assessments

- Encrypted payment terminals or hosted checkout pages

- Regular security updates

- Fraud detection and prevention tools

Providers that push PCI compliance to the background could expose your business to penalties and unnecessary risk.

Test Customer Support Responsiveness

Don’t wait until your funds are frozen to find out if the support team is responsive. Reach out before signing up to evaluate:

- Speed of response (chat, email, or phone)

- Technical knowledge

- Availability (24/7 support is ideal for eCommerce)

Pro tip: Try calling during off hours (like a weekend or late evening) and see how long it takes to connect with a live agent.

Read Independent Reviews

Go beyond testimonials on the company’s site. Look for reviews on popular forums or other reputable review sites, such as:

- Trustpilot

- G2

- Better Business Bureau

- Reddit (r/smallbusiness or r/entrepreneur)

Pay attention to common complaints like surprise fees, fund holds, or bad customer service.

Match Risk Level With the Right Provider

Some providers flat-out reject high-risk businesses, while others specialize in them. If you fall into one of the following categories, you need a high-risk merchant account provider:

- Subscription services

- CBD or supplements

- Travel booking

- Adult entertainment

- Dropshipping

Providers like PayKings, SMB Global, and Soar Payments are known for working with high-risk industries.

Final Checklist Before Signing

Before committing, make sure you:

- Understand all fees: setup, monthly, transaction, chargebacks, PCI, etc.

- Know the contract terms: length, termination policy, renewal conditions

- Have clear points of contact: sales, support, and compliance

- Get everything in writing: especially custom rates

Pro Tip:

The “cheapest” provider isn’t always the best. What matters is total value: support, tools, scalability, and pricing combined. Sometimes paying a slightly higher rate saves you hundreds or thousands in lost time, downtime, or disputes.

Alternatives to Merchant Accounts (and When They Make Sense)

While traditional merchant accounts offer unmatched control, security, and scalability, they’re not always the right fit for every business, especially in the early stages. If you’re a startup, freelancer, or side hustler looking for faster onboarding or fewer technical requirements, it’s worth considering the available alternatives.

Let’s walk through the most popular merchant account alternatives, the pros and cons of each, and when they make more sense than a full-blown merchant setup.

#1: Payment Service Providers (PSPs)

Payment Service Providers — also known as third-party payment processors — act as intermediaries between your business and your customers’ card issuers. Unlike merchant accounts, they aggregate your transactions with many other businesses under a single master account.

Popular PSPs:

- PayPal

- Stripe

- Square

- Shopify Payments

When They Make Sense:

- You’re just launching your business

- You process under $10,000/month

- You want fast setup and instant approval

- You need basic online or in-person payment options

Pros:

- Instant approval, no underwriting

- Flat-rate pricing (e.g., 2.9% + $0.30)

- Easy to integrate with eCommerce platforms

- Great for solopreneurs and micro-businesses

Cons:

- Higher fees than custom merchant accounts

- Limited control over chargebacks and disputes

- Account holds/freezes are more common

- Less scalability for growing companies

#2: Mobile Payment Apps

Mobile-first tools like Zelle, Venmo for Business, and Cash App are popular among freelancers, food vendors, and local service providers.

These apps are not designed for traditional eCommerce but work well for casual transactions.

When They Make Sense:

- You operate in a peer-to-peer or service-based model

- You don’t need invoices, subscriptions, or reporting features

- You’re not worried about chargebacks or compliance

Pros:

- No hardware required

- Free or low transaction fees

- Instant transfers in many cases

- Easy for customers to use

Cons:

- Not PCI compliant for formal business use

- No customer dispute resolution systems

- Often limited to mobile-only functionality

- May breach terms of service if used commercially without approval

#3: Payment Aggregators via eCommerce Platforms

If you’re using Shopify, BigCommerce, WooCommerce, Wix, or Squarespace, these platforms often bundle payments directly into your website builder through services like Shopify Payments, Wix Payments, or WooPayments.

When They Make Sense:

- You’re launching an online store quickly

- You want a plug-and-play solution with minimal tech work

- You’re okay with using the platform’s preferred processor

Pros:

- Integrated dashboards (orders + payments)

- Streamlined checkout for customers

- Predictable flat-rate fees

- No need to deal with third-party providers directly

Cons:

- Locked into their ecosystem

- Switching payment providers may require full site rebuild

- Flat fees can become expensive at scale

#4: All-in-One Invoicing and Payment Platforms

For freelancers, consultants, and B2B businesses, platforms like FreshBooks, Wave, Bonsai, or HoneyBook offer invoicing, contracts, and payment acceptance all in one place.

When They Make Sense:

- You bill clients via email or PDF invoices

- You need contracts, proposals, and payments in one workflow

- You’re not doing in-person or POS-based sales

Pros:

- Professional client experience

- Automation for recurring invoices

- Some platforms support ACH transfers (lower fees)

- Great for solo professionals

Cons:

- Less suitable for high-volume, retail, or eCommerce sales

- Not optimized for physical products or inventory

- Limited fraud protection compared to full merchant accounts

#5: Crypto Payment Gateways

For digital-savvy audiences, cryptocurrency payment gateways like Coinbase Commerce, BitPay, or NOWPayments allow you to accept Bitcoin, Ethereum, and other coins as payment.

When They Make Sense:

- You cater to a tech-forward or international audience

- You want to bypass traditional banking and fees

- You understand crypto volatility and regulations

Pros:

- No chargebacks

- Lower transaction fees than traditional cards

- Access to global markets

Cons:

- Price volatility (your $100 could be $85 tomorrow)

- Less mainstream adoption

- Complex tax implications

- Not accepted by most accounting platforms or banks

Finally, that’s all you need to know about a merchant account.

Use Square for WordPress [No Merchant Account Needed]

If you want to skip merchant account setup entirely, connect Square to your WordPress site with WP EasyPay. This powerful plugin lets you accept online payments, donations, and subscriptions quickly — no coding or third-party merchant account required.

WP EasyPay offers secure transactions, real-time reporting, and simple recurring billing, all inside WordPress. It’s a smart choice for small businesses, nonprofits, and freelancers who want fast setup and lower fees.

Click here to download the plugin and start accepting credit card payments on WordPress today with WP EasyPay and Square — it’s easy, affordable, and built to grow with you.